Accepting online payments by credit card in Cambodia

How can I receive online credit card payments in Cambodia?

Over the past four years, we have researched and implemented a wide range of payment solutions for our Cambodian customers and our own projects. In this article, we share an up-to-date summary of our experiences with the available solutions.

This overview focuses on services that allow receiving international credit card payments to a Cambodian bank account. We will not cover P2P money transfer services or e-wallets such as Wing, Pi Pay or PayGo in this article. While most available payment solutions require a registered Cambodian business or organization, iPay88 also accepts startups that have submitted their business registration and are waiting for the approval.

In 2017, we have released GetLoy Payments, a payment solution integration platform for Cambodian payment gateways providing a one-stop API to accept payments in Cambodia. One of the most popular features of GetLoy is the ability to send payment links thru e-mail, Facebook Messenger or other IM to request payment. Read more in our press release.

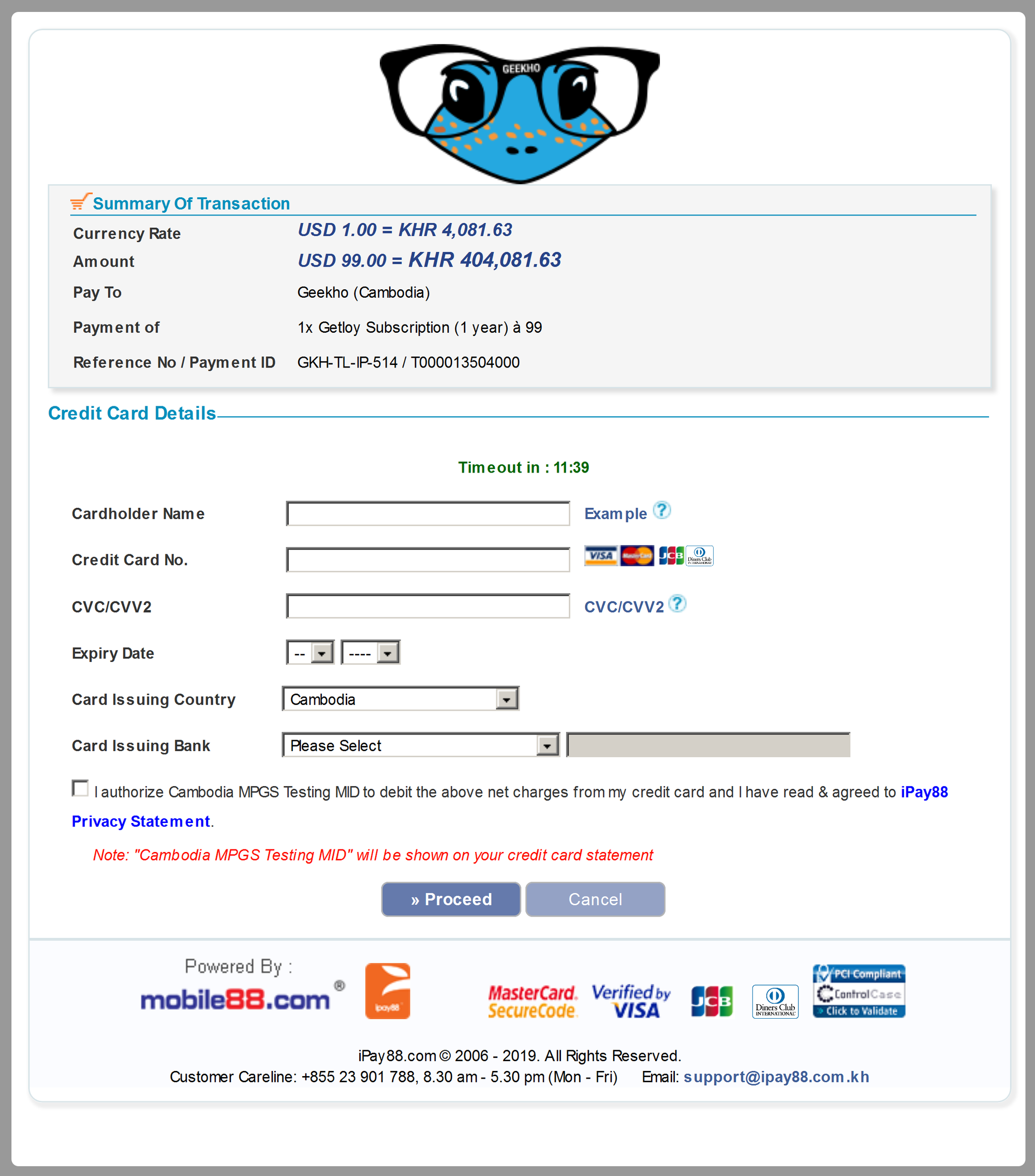

iPay88

iPay88 is a payment integrator headquartered in Malaysia that has expanded to several countries across Southeast Asia. In 2015, they opened an office in Cambodia. Their merchants processed over 52 million transactions in 2018.

As an integrator, iPay88 provides numerous international and local payment options - besides Visa and MasterCard, iPay88 supports a range of Cambodian e-wallets and transfers from Cambodian bank accounts. They also connect to Alipay, a leading payment platform for Chinese customers.

Merchants can use all of iPay88's supported payment options without having to sign up for each payment provider separately. iPay88 commits to processing merchant applications within 3-5 working days after receiving the complete application documents - the fastest processing time in the industry to our knowledge.

iPay88 has startup-friendly merchant requirements - businesses can already apply for a merchant account while their business registration at the Ministry of Commerce is still being processed. Requirements are stricter for NGO's however - they need to be registered for at least 12 months to be eligible for a merchant account.

The payment interface of iPay88 is easy to use, but not as modern as PayWay's.

Transaction fees are 3.5% for debit/credit card transactions, 2.5% for online banking transfers and 1.5% for e-wallets. iPay88 also charges a one-time setup fee of $300 and an annual maintenance fee of $360. A deposit or rolling reserve may be required depending on their risk assessment of the merchant's business.

Unlike other payment providers, iPay88 charges a refund fee of $2 per transaction or 0.2% of the transaction volume for transactions over $1000.

PayWay by ABA Bank

ABA Bank introduced PayWay in July 2017. The platform supports Visa, MasterCard and UnionPay.

Besides debit and credit cards, PayWay also supports payments directly from ABA bank accounts via their mobile banking app (ABA Pay). This can be an interesting option for merchants with domestic customers, as ABA Pay payments received via PayWay are credited to the merchant's bank account instantly and incur no fees.

Unlike the MiGS-based payment solutions, PayWay provides a modern, intuitive payment interface that opens in an iframe on the merchant’s checkout page. The interface is customized for each merchant with the merchant’s logo and the colour matching the merchant’s website. The looks of the interface help to gain the trust of customers used to the look of payment interfaces of international payment providers like PayPal or Stripe.

Beautiful as it is, the user interface is also a bit of a golden cage, as PayWay does not allow their merchants to use custom payment interfaces. ABA Bank has also imposed a growing number of requirements on design aspects of the checkout process and the merchant's website in general. These requirements include things like the exact wording of the payment option and the payment button (down to the capitalization of each word), and the bank has recently started requiring new merchants to add a banner to the footer of the site saying that the site supports payments via PayWay.

Like the payment interface, PayWay’s merchant back-end has an intuitive design, allowing merchants to gain a quick overview of pending and completed transactions, and to refund payments with a few clicks. Online refunds are not supported for all issuing banks, however – if the customer’s bank is not supporting this function, the refund needs to be requested by email to ABA Bank instead.

ABA Bank's payment system is hosted in Cambodia, and while the situation has improved over the last years, the system availability is still not at the level of international payment providers.

The bank has put efforts into streamlining the onboarding procedure for PayWay merchants, which typically takes a few weeks to complete. Prospective merchants reported however that the process can still be frustrating for NGOs (who generally have a hard time getting a merchant account in Cambodia) and companies whose business model does not fit the standard boxes.

PayWay’s pricing is competitive - ABA Bank charges an onboarding fee of $100, and there is no monthly fee normally, although the bank reserves the right to charge one for merchants with less than 5 transactions per month. While deposits are normally also waived for businesses, some NGOs were required to deposit as much as $1000. The transaction fees differentiate between cards issued by Cambodian and international banks and are at the same level as iPay88. Payments received from ABA customers via ABA Pay are free of charge.

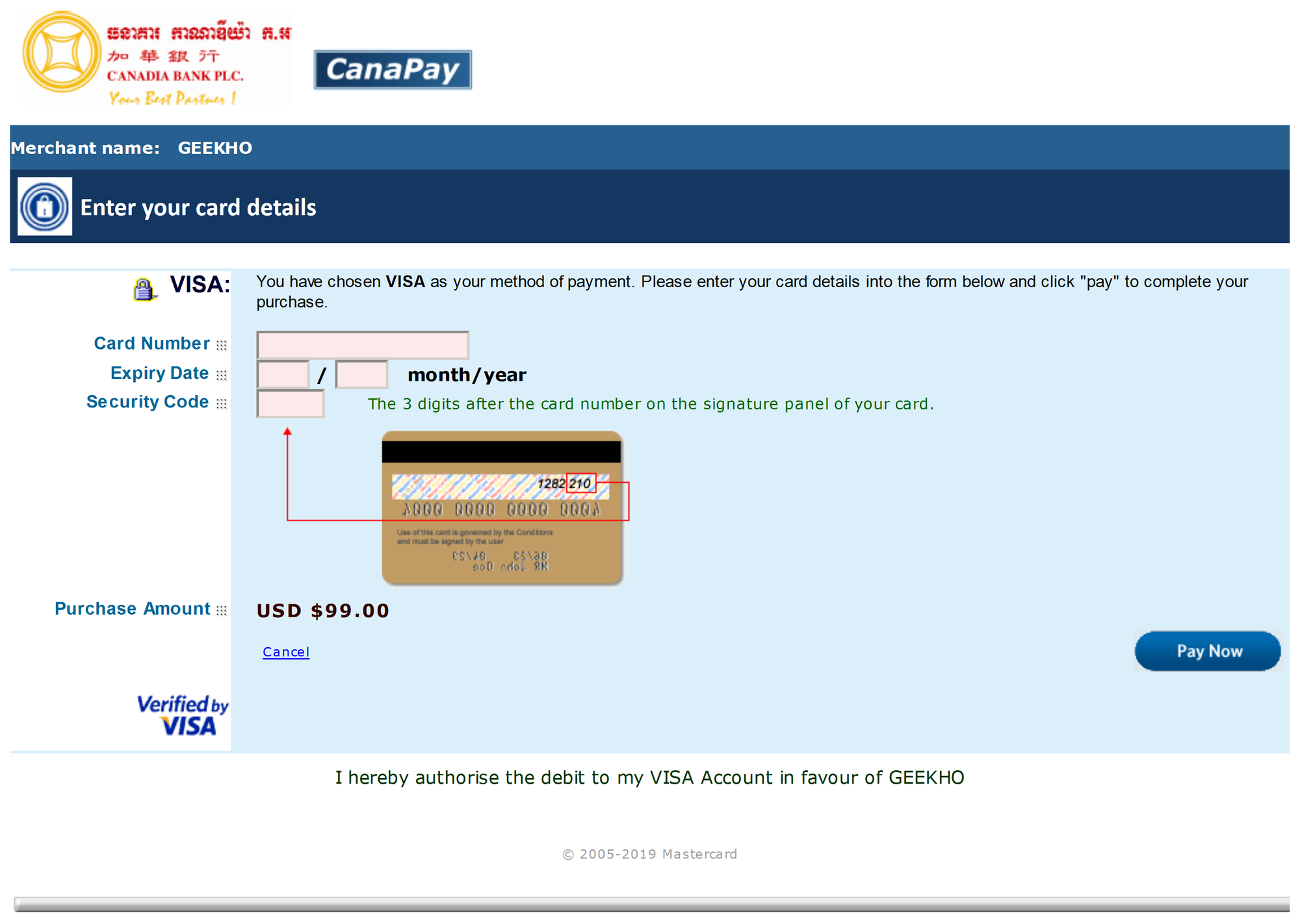

MiGS gateways: Cathay United, Canadia and ACLEDA

Cathay United Bank’s Payment Gateway Service, Canadia Bank’s Online Payment Gateway Service and ACLEDA Bank’s E-Commerce Payment Gateway are all based on the MasterCard Internet Gateway Service (MiGS) operated by MasterCard in Australia. MiGS support online payments with MasterCard, Visa and JCB.

Because of this common platform, the payment processing forms and merchant back-ends are virtually identical for all three banks, except for the different logos.

One issue of the MiGS-based payment solutions is not related to the MiGS platform, but to the merchant onboarding procedures of the banks, which can be frustratingly slow for potential merchants. From our experience, it typically takes several months (in some cases as long as half a year) to set up a new merchant account.

A major downside of MiGS itself is the outdated look of the user interface both for payment processing and the merchant backend, which does not fit well with the design of modern websites and does not help to instil trust in the payment process on the side of the customer. The payment interface is also not responsive, making it difficult to complete a transaction from a mobile phone.

The default user interface for the payment processing part can be fully customized using “mode 2 transactions”. This, however, requires the merchant to create their own credit card capturing form, and to process credit card information on their website, meaning that the merchant must implement rigorous security measures to prevent hackers from stealing their customers’ credit card information.

MiGS offers a highly interesting feature for merchants such as accommodations that only want to charge their customers’ credit cards in case of no-shows and otherwise settle the transaction with cash payments. For so-called “mode 3a/3b transactions”, the payment is processed in two steps – Authentication and Payment. In the Authentication step, the customer enters the credit card details and approves the transaction. At this point, the amount is only getting blocked in the customer’s account. To make the payment (e.g. in case of a no-show), the merchant can perform the Payment step. If the customer instead pays in cash, the merchant can void the Authentication to release the blocked amount in the customer’s account. Like the custom payment processing interface, however, implementing mode 3a/b transactions is complex and requires a highly secure website.

The MiGS Virtual Payment Client also supports several “Advanced Merchant Administration” (AMA) transactions, allowing merchants to refund or void transactions through the MiGS API. From our experience, the Cambodian banks offering MiGS-based online payment solutions do not support all AMA transactions, so merchants interested in using them should inquire about the availability with the bank of their choice.

Bongloy

First announced in 2014, Bongloy has been in public beta since early 2019.

The service currently only supports payments via UnionPay, which makes Bongloy infeasible as the only payment provider for most use cases.

The idea behind Bongloy was to create an API-based online payment solution for Cambodia to accept both domestic and international credit cards. Bongloy’s API is compatible with Stripe, meaning that support for Bongloy can be added to e-commerce platforms that already support Stripe by changing the URLs used in the Stripe integration. Bongloy maintains forks of some popular Stripe integrations on their GitLab account, but most of them are marked as deprecated.

The merchant onboarding for Bongloy is straightforward and can conveniently be completed online by registering and uploading scans of the required documents. Bongloy also accepts Cambodian nationals without a registered business as merchants.

There are no setup charges or monthly/annual fees, but Bongloy requires a deposit from its merchants that can be in the four-digit USD range depending on the business profile. Credit card transaction fees are the lowest of all payment providers at 2.9% plus $ 0.20 per transaction. There is also a small fee per payout to the merchant's bank account.

Bongloy has several innovative features like Bongloy Connect, which can e.g. be used for online marketplaces to take payments on behalf of the individual sellers and automatically deduct the platform fee from the payment.

Unlike other financial service providers in Cambodia, Bongloy demonstrates a commitment to transparency by providing a public sandbox for the API and a public status page showing the service availability over the last 30 days. It is also the only payment provider in the Kingdom that discloses it's API documentation publicly - a clear statement against the security by obscurity approach that too many Cambodian financial service providers still rely on.

2C2P Payment Gateway

2C2P is a payment service provider based in Singapore. Its Cambodian subsidiary 2C2P (Cambodia) Co., Ltd. was incorporated in 2012.

While there is little advertisement of their merchant services in Cambodia, 2C2P is for example listed as a supported payment method for eZee Reservation, an accommodation reservation system popular for smaller Cambodian hotels and guest houses.

2C2P's Payment Gateway (PGW) supports debit/credit card payments with Visa, MasterCard, JCB, American Express, Discover, Diners Club and UCB, more than any other provider in Cambodia.

They also have the most restrictive merchant eligibility criteria however – merchants need to process about USD 100,000 (THB 3 million) per month.

Transaction fees are at 3.25%, plus 0.25% and USD 50 for the settlement to the merchant's Cambodian bank account. While the base fees are thus similar to those of other payment providers, merchants meeting the transaction volume requirements of 2C2P will likely be able to negotiate better rates with iPay88 and PayWay.

Summary

The choice of payment providers available in Cambodia for accepting international online debit/credit card payments has increased a lot over the last years. Picking the right one for your business or organisation largely depends on factors like your expected monthly payment volume, your official registration status and the country of origin of your customers.

Once you have picked your payment provider(s), our payment integration solutions GetLoy can help you to connect them to your website in minutes with secure and robust plugins for platforms like WooCommerce and PrestaShop.

If you are unsure about which payment provider is the right one for you, or how to connect to connect it to your website, feel free to contact us via the live chat on geekho.asia or drop us an email - we also welcome suggestions or comments.